admin

HELOC Loans Unlocked: How Do They Work?

Tapping into Home Equity: A Solution for Your Financial Challenges

Tapping into Home Equity: A Solution for Your Financial Challenges

Facing pressing financial needs like urgent home improvements or the need to consolidate debts can be daunting, especially when considering using your home’s equity. The world of Home Equity Lines of Credit (HELOC) is filled with complex terms and fluctuating interest rates, often leading to confusion and worry. The thought of hidden costs and the risk to your most valuable asset – your home – can make the decision to choose a HELOC an overwhelming one.

This guide is designed to simplify HELOCs, providing clear and concise insights into how they work and how they can serve as a viable financial tool. Whether you’re looking to upgrade your home or alleviate financial pressures, we offer the guidance you need to navigate this process with confidence. If you’re ready to harness the potential of your home equity, apply now for a financial solution that meets your needs.

Understanding HELOC: Harnessing Your Home Equity

When it comes to utilizing the equity in your home, a Home Equity Line of Credit (HELOC) stands out as a flexible and often-used option. Understanding how a HELOC functions is key to deciding whether it’s the right financial tool for you.

A HELOC is a type of loan where your home serves as collateral, offering you access to a revolving credit line. Unlike a traditional lump-sum loan, a HELOC allows you to borrow up to a certain amount during a “draw period,” usually 5 to 10 years, and pay back only what you use.

How HELOCs Work:

- Draw Period and Repayment Phase: During the draw period, you can borrow funds as needed, often with the flexibility to make interest-only payments. Following this, the repayment phase begins, where you pay back the borrowed amount along with interest over a set period.

- Interest Rates: HELOCs typically have variable interest rates, meaning the rate can change over time based on market conditions. This aspect requires careful consideration, as it can affect your monthly payments.

- Access to Funds: Most HELOCs provide easy access to funds through checks or a card linked to the credit line, making it a convenient option for ongoing expenses.

Understanding these key features of a HELOC can help you assess its suitability for your financial situation. Whether for home renovations, education expenses, or debt consolidation, a HELOC offers a flexible approach to borrowing against your home equity, but it’s vital to consider the potential impact on your long-term financial health.

Key Criteria for HELOC Approval

Securing a Home Equity Line of Credit (HELOC) involves meeting specific lender requirements. Here’s a breakdown of the essential qualifications you need to be aware of for HELOC approval:

Home Equity as a Foundation

The amount of equity in your home is a critical factor for HELOC eligibility. Typically, lenders require you to have 15% to 20% equity, which is the difference between your home’s current market value and your mortgage balance.

The Role of Your Credit Score

Your credit score significantly influences your HELOC application. A higher score often means better interest rates and terms. While lower scores may not disqualify you, they can impact the loan’s conditions.

Debt-to-Income Ratio (DTI) Considerations

Lenders assess your DTI ratio, a measure of your monthly debt payments against your gross monthly income. A lower DTI ratio suggests to lenders that you’re more likely to manage the additional debt of a HELOC.

Income Stability for Loan ConfidenceDemonstrating steady and reliable income is essential. It reassures lenders of your capacity to repay the borrowed amount.

Understanding and meeting these criteria is crucial for HELOC approval. Each lender may have varying requirements, so it’s beneficial to compare different offers. Ensuring these qualifications align with your financial situation and goals is key to a successful HELOC application.

Credit Score Impact on HELOC Approval

The role of your credit score in securing a Home Equity Line of Credit (HELOC) is pivotal. This section delves into how your credit score influences the HELOC process, including the possibilities for those with lower scores.

Understanding the Credit Score Influence:

- Higher Scores, Better Terms: A higher credit score typically opens the door to more favorable interest rates and loan terms. Lenders see higher scores as an indicator of reliability and lower risk.

- Lower Scores and HELOC Options: Having a lower credit score doesn’t necessarily mean you can’t get a HELOC, but it may affect the terms and conditions of your loan. Lenders might offer a higher interest rate or a lower borrowing limit to offset the perceived risk.

- Special Considerations: For those with a credit score around 580, HELOC options may be limited, but they aren’t non-existent. It’s crucial to shop around and discuss with lenders to find potential opportunities.

- No-Credit-Check Options: While rare, some lenders might offer HELOCs without a credit check, usually at the cost of less favorable loan terms.

Your credit score plays a significant role in determining your eligibility and the terms of a HELOC. It’s advisable to review your credit score and understand its impact before applying for a HELOC. Improving your credit score, if needed, can be beneficial in securing better loan terms. Regardless of your credit situation, exploring all available options and speaking with different lenders can help you find a suitable HELOC solution.

Exploring Refinancing in Home Equity Loans

Refinancing your home equity loan or HELOC can be a strategic financial decision, offering opportunities to adjust to more favorable terms or rates. It’s a process that requires a careful evaluation of your current loan situation against the backdrop of your long-term financial goals.

Refinancing Your Home Equity Loan

When it comes to refinancing a home equity loan, the main objectives are usually to secure lower interest rates or to change the loan’s terms to better suit your current financial situation. Key factors to consider include the prevailing interest rates, your current credit score, and the outstanding balance on your loan. The ultimate aim is to ensure refinancing leads to tangible benefits such as reduced payments or a more manageable loan term.

HELOC vs. Cash-Out Refinance

Refinancing a HELOC may involve modifying the terms of your existing credit line or integrating it into your primary mortgage. On the other hand, a cash-out refinance involves adjusting your primary mortgage and extracting additional funds based on your equity. This option differs from a HELOC and should be weighed for its long-term impact and current mortgage rate implications.

Refinancing within the home equity space is a nuanced decision that should align with both your immediate and future financial needs. It’s advisable to consult with financial advisors to navigate these options effectively.

Tax Benefits of a HELOC

- Potential Tax Deductibility: Interest paid on a HELOC may be tax-deductible if used for qualifying expenses like home improvements.

- Home Improvement Advantage: Using HELOC funds for buying, building, or substantially improving your home typically qualifies for tax deductions.

- Varying Based on Use: Tax deductibility depends on how you use the HELOC funds; personal expenses like debt consolidation usually don’t qualify.

It’s important to consult a tax professional for personalized advice, as tax laws can be complex and vary based on individual circumstances.

Timeline and Process for Obtaining a HELOC

Understanding the timeline for obtaining a Home Equity Line of Credit (HELOC) is crucial in planning your financial steps. This section provides insight into the typical duration and the process involved in securing a HELOC.

The process of getting a HELOC usually involves several stages, each contributing to the overall timeframe:

- Application and Approval: Initially, you’ll need to apply with a lender, providing necessary documentation such as proof of income, credit information, and details about your home’s equity. The approval process can vary, typically ranging from a few days to several weeks, depending on the lender’s requirements and your financial situation.

- Appraisal and Valuation: Part of the process may include an appraisal of your home to determine its current market value. This appraisal is a key factor in deciding how much you can borrow and can add time to the approval process.

- Finalizing the Loan: Once approved, there will be a period for finalizing the loan terms and paperwork. This stage includes reviewing and signing loan agreements, which can be relatively quick but is dependent on how promptly you and the lender complete the necessary steps.

- Access to Funds: After all the paperwork is finalized, you’ll have access to the funds. Some lenders may offer immediate access, while others might have a brief waiting period.

Overall, the timeline for obtaining a HELOC can range from a few weeks to a couple of months. Planning ahead and understanding this process can help ensure a smooth experience. It’s also important to work with a responsive lender and to provide all required information promptly to expedite the process.

Can I Sell My House if I Have a HELOC?

Yes, you can sell your house even if you have an active Home Equity Line of Credit (HELOC). However, there are important considerations and steps involved in this process.

When you decide to sell your home with an active HELOC, the outstanding balance of the HELOC must be paid off as part of the sale process. Here’s how it typically works:

- Paying Off the HELOC: The outstanding balance on your HELOC is usually paid off using the proceeds from the sale of your house. This is often handled as part of the closing process.

- Closing the HELOC Account: Once the balance is paid off, the HELOC account is closed. This step is crucial to release the lien on the home, allowing for a clear transfer of the property title to the new owner.

- Managing Remaining Proceeds: If there are any remaining proceeds from the sale after paying off the HELOC and any other mortgages or liens, these funds are typically returned to you.

Selling a home with a HELOC requires careful financial planning and coordination with your lender and real estate professionals. It’s important to understand how the sale impacts your financial obligations and to ensure that the HELOC is fully accounted for in the sale process. By managing these details effectively, you can smoothly transition to selling your home, even with an active HELOC.

Deciding Between HELOC and Home Equity Loan

When choosing how to leverage your home’s equity, consider these key differences between HELOCs and traditional home equity loans:

HELOC:

- Offers a flexible credit line for varied borrowing needs.

- Typically has a variable interest rate.

- Suitable for ongoing expenses or projects.

Home Equity Loan:

- Provides a one-time lump sum with a fixed interest rate.

- Ensures predictable monthly payments.

- Ideal for single, large expenses.

Your choice between a HELOC and a home equity loan should be based on your specific financial needs, preference for payment predictability, and comfort with interest rate variations.

Exploring Other Quick Cash Solutions

In addition to HELOCs, there are several other financial options available for obtaining quick cash. Understanding these alternatives can help you make a more informed decision, especially if you’re weighing the pros and cons of taking out a HELOC. Here’s a brief overview of some immediate financial solutions and income strategies without debt:

Immediate Financial Solutions:

- Home Equity Loans: Use home equity for loans with lower interest rates, but be mindful of the foreclosure risk.

- Payday Loans: Provide instant cash but typically come with very high interest rates.

- Personal Loans: Suitable for those with good credit, offering lower interest rates.

- Credit Card Cash Advances: Easily accessible but can be expensive due to high fees and interest rates.

- Title Loans: Quick access to cash using your vehicle as collateral but with the risk of losing your vehicle.

- Peer-to-Peer Loans: Flexible lending options with varying rates based on community-based platforms.

- Pawn Shop Loans: Immediate funds in exchange for valuable items as collateral.

- 401(k) Loans: Borrow from retirement savings without a credit check but with a potential impact on retirement funds.

- New Credit Cards with Introductory Offers: Useful for short-term expenses, offering introductory periods with low or no interest.

Wells Fargo Reflect® | 0% APR for 21months (Credit Score 670+)

»

|

iCash Loans | Get a Loan Today

»

|

Brigit | Build Your Credit and Your Savings

»

|

BadCreditLoans.com | Quick Loans up to $10,000

»

|

Income Strategies Without Debt:

- Borrowing from Family and Friends: Could offer flexible, interest-free loans but may impact personal relationships.

- Selling Personal Items: Convert belongings into cash, though it can require time and effort.

- Seeking Community Assistance: Look for non-repayable support from charities or government programs.

- Side Gigs or Freelancing: Generate extra income without the commitment to a traditional loan.

Each of these alternatives comes with its own set of advantages and considerations. It’s important to assess your individual financial situation, the urgency of your needs, and your ability to meet potential repayment obligations before choosing the right option for you.

FAQ: Addressing Common HELOC Questions

In this section, we tackle some frequently asked questions about Home Equity Lines of Credit (HELOCs) to provide clarity and assist in your decision-making process.

Is it hard to get approved for a HELOC?

Approval for a HELOC depends on factors like your home equity, credit score, and debt-to-income ratio. While higher credit scores and more home equity generally ease the process, having lower scores and less equity doesn’t automatically disqualify you.

How does a HELOC loan work for those with bad credit or a credit score of 580?

Obtaining a HELOC with a lower credit score, such as 580, can be challenging, but it’s not out of reach. Lenders may offer HELOCs at higher interest rates or with specific conditions to mitigate the risk of lower credit scores.

Is a home equity loan a good idea for homeowners?

A home equity loan can be beneficial for significant, one-off expenses, thanks to fixed interest rates and predictable repayments. However, it’s crucial to evaluate its long-term effects on your home equity and financial situation.

Are there options for a home equity loan with no credit check?

Home equity loans typically involve a credit check as part of the approval process. Some lenders may provide options for those with flexible credit requirements, but these usually come with different terms.

These answers offer a foundational understanding of HELOCs, helping you navigate through various aspects of this financial tool. For more specific guidance, consulting with financial professionals or your lender is recommended.

Conclusion: Is a HELOC the Right Choice for You?

As we conclude our comprehensive guide on Home Equity Lines of Credit (HELOCs), it’s important to reflect on whether this financial tool aligns with your unique needs and circumstances. A HELOC offers flexibility and can be a powerful resource for leveraging the equity in your home, but it also requires thoughtful consideration of the potential impact on your long-term financial health.

Key Takeaways:

- A HELOC provides a flexible line of credit based on your home equity, but it comes with variable interest rates and terms that can affect your financial stability.

- Understanding your eligibility, the tax implications and the differences between a HELOC and other loan options like home equity loans is crucial.

- Consider your current financial situation, future goals, and how comfortable you are with the associated risks and benefits of a HELOC.

Ultimately, the decision to choose a HELOC should be based on a careful evaluation of how it fits into your overall financial plan. It’s not just about accessing funds; it’s about making a strategic choice that supports your financial objectives both now and in the future.

Take Control of Your Financial Future

Considering a HELOC or exploring financial alternatives? Consult with a financial advisor for advice tailored to your specific needs, ensuring you choose the best path for your financial future.

Have insights or experiences with HELOCs? Sharing your story could aid others in their decisions. Don’t hesitate—contact a financial advisor today to take a confident step towards your financial goals.

Caught in a Bind? Know Your Emergency Financial Options

Borrow from Retirement With A 401k Loan: A Comprehensive Guide

Navigating 401k Loans: Balancing Today’s Needs with Tomorrow’s Retirement

In times of financial stress, the idea of borrowing from your 401k can seem like an immediate solution. However, this decision can have significant long-term effects on your retirement savings. The challenge lies in addressing your current financial needs without compromising your future financial stability.

While a 401k loan might provide the quick financial relief you need, it’s crucial to consider how it could set back your retirement plans. It’s a balance between fulfilling immediate financial obligations and preserving your nest egg for the future.

This guide is designed to simplify the process of borrowing from your 401k. We’ll help you understand the loan terms, evaluate its impact on your retirement, and guide you through making a well-informed decision.

Understanding 401k Loans: The Essentials

A 401k loan allows you to access funds from your retirement account, subject to certain rules. Here’s a brief overview:

- Borrowing Limits: You’re generally allowed to borrow up to 50% of your vested account balance, up to $50,000.

- Repayment Terms: Repayment typically spans up to five years, often requiring regular quarterly payments.

- Interest: The interest paid on the loan is credited back into your 401k account.

Grasping these fundamental aspects is key in evaluating whether a 401k loan aligns with your financial strategy, especially considering its impact on your long-term retirement planning.

Understanding the Financials: 401k Loan Interest and Payments

Borrowing from your 401k involves more than just accessing your funds; it’s crucial to understand the financial implications, particularly the interest rates and repayment process. This section breaks down these key aspects, helping you to navigate the cost considerations of a 401k loan.

Interest Rates on 401k Loans

The interest rate for a 401k loan typically follows the plan’s guidelines, generally based on the prime rate with an additional percentage. Unique to this loan type, the interest paid goes back into your 401k account, effectively letting you ‘pay yourself back’ with interest.

Calculating Loan Payments

Using a 401k loan calculator can provide a clear understanding of your repayment obligations. It takes into account the loan amount, interest rate, and repayment term, offering insights into your monthly payments and the total amount you’ll end up paying back. This tool is essential for assessing the loan’s impact on both your immediate finances and your long-term retirement savings.

Exploring the Reasons: Why Borrow from Your 401k?

Deciding to take a loan from your 401k shouldn’t be made lightly. Understanding the various reasons people choose to borrow from their retirement savings can help you evaluate if it’s the right decision for your circumstances.

People opt for 401k loans for a variety of reasons, each with its own set of considerations:

- Home Purchase: Many use 401k loans for significant expenses like buying a home, taking advantage of not having to qualify for a bank loan or deal with potential credit issues.

- Debt Consolidation: Some find 401k loans useful for consolidating high-interest debt, potentially leading to lower overall interest payments.

- Emergency Expenses: Unexpected costs, such as medical bills or urgent home repairs, can lead individuals to tap into their 401k.

- Education Costs: Funding education, whether for themselves or family members, is another common reason for a 401k loan.

While these reasons are valid, it’s crucial to balance the immediate need for funds with the potential long-term impact on your retirement savings. A 401k loan might solve a current financial problem, but it could also diminish your future financial security. Understanding why you need the loan and considering all possible alternatives is key to making a sound financial decision.

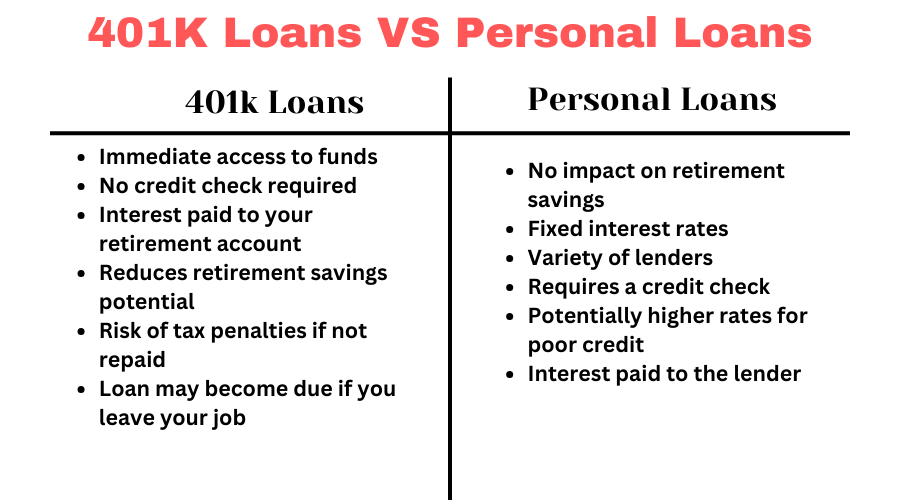

Financial Crossroads: 401k Loans vs. Personal Loans

When considering a loan, it’s important to compare 401k loans with personal loans, as each has its own set of benefits and drawbacks. This section helps you understand these differences to make an informed choice based on your financial situation.

When choosing between a 401k loan and a personal loan, consider factors like the impact on your retirement savings, interest rates, and how your employment status might affect your ability to repay a 401k loan. Your decision should align with both your immediate financial needs and your long-term financial health.

The Payback Plan: Navigating 401k Loan Repayment

Understanding the repayment process of a 401k loan is essential for managing your finances effectively. Here’s what you need to know about paying back a 401k loan:

- Repayment Timeline: Generally, 401k loans must be repaid within five years. However, if the loan is used for a home purchase, this period might be extended.

- Payment Frequency: Repayments are usually required to be made at least quarterly, but many plans ask for monthly payments.

- Direct from Paycheck: Repayments are often deducted directly from your paycheck, making the process convenient and ensuring timely payments.

- Interest Repayment: The interest you pay on the loan is credited back into your 401k account. It’s like paying the interest to yourself, which can help offset some of the impacts of borrowing from your retirement funds.

By staying informed about the repayment process, you can ensure that your 401k loan doesn’t become a financial burden. Remember, timely repayment is crucial to avoid taxes and penalties and to keep your retirement savings on track.

Exploring Financial Alternatives to 401k Loans

When considering different financial solutions, it’s beneficial to examine a range of options beyond 401k loans. Each alternative offers distinct advantages and risks:

Immediate Financial Solutions:

- Payday Loans: Offer immediate cash but usually with high costs.

- Personal Loans: Ideal for those with good credit, offering lower interest rates and requiring proof of repayment ability.

- Credit Card Cash Advances: Easily accessible, yet tend to have high interest rates and fees.

- Title Loans: Quick cash using your vehicle as collateral, but risk losing the vehicle.

- Peer-to-Peer Loans: Flexible, community-based lending with varying rates.

- Home Equity Loans: Based on home equity, offering lower rates but carrying the risk of foreclosure and requiring a longer approval process.

- HELOC (Home Equity Line of Credit): Offers adaptable access to funds through variable interest rates, making it perfect for recurring expenses.

- Pawn Shop Loans: Provide quick access to cash with valuables as collateral, but come with the risk of losing your items.

- Getting a New Credit Card: Useful for short-term expenses with 0% introductory offers, but consider the standard rate post-introductory period.

|

Brigit | Build Your Credit and Your Savings

»

|

Wells Fargo Reflect® | 0% APR for 21months (Credit Score 670+)

»

|

|

iCash Loans | Get a Loan Today

»

|

BadCreditLoans.com | Quick Loans up to $10,000

»

|

Income Strategies Without Debt:

- Borrowing from Family and Friends: Can offer low- or no-interest loans but may affect personal relationships.

- Selling Personal Items: A way to raise funds without incurring debt, though it may take time.

- Seeking Community Assistance: Non-repayable support from charities or government programs for those in financial distress.

- Exploring Side Gigs: Part-time work or freelancing to earn extra income without taking on loans.

Each alternative has its advantages and drawbacks. Carefully consider factors like interest rates, repayment terms, and the potential impact on your financial health to make a decision that suits your immediate needs and long-term financial goals.

Weighing the Scales: The Benefits and Drawbacks of 401k Loans

When it comes to taking out a 401k loan, understanding both its advantages and disadvantages is crucial for making an informed decision. Here we delve into an in-depth analysis of the pros and cons.

Pros:

- Quick access to funds without a credit check.

- Simple application process.

- Interest paid into your own 401k account.

- No impact on credit score.

Cons:

- Can reduce future retirement savings.

- Full repayment often required if you leave your job.

- Missed investment growth on borrowed funds.

- Potential taxes and penalties for non-repayment.

When considering a 401k loan, balance these factors against your current financial needs and long-term retirement goals. It’s crucial to ensure you can manage repayment without adversely affecting your future financial health.

Addressing Common 401k Loan Queries: Your Questions Answered

Navigating the details of a 401k loan involves addressing some key questions that borrowers commonly have. Here’s a closer look at these inquiries.

Will my employer know if I take a 401k loan?

Your employer will typically be aware of a 401k loan since these loans are part of the retirement plan they manage. However, this information is usually just a part of standard plan administration and doesn’t generally impact your job.

How long does it take for a 401k loan to be approved?

The approval time for a 401k loan can vary, often ranging from a few days to a couple of weeks. This depends on the specific procedures and rules of your 401k plan.

How can I borrow from my 401k without penalty?

To avoid penalties when borrowing from your 401k, it’s crucial to adhere to the repayment terms. Typically, you need to repay the loan within five years to steer clear of any penalties.

How many months do I have to pay back a 401k loan?

You’re usually required to repay a 401k loan within 60 months or five years. Some plans might offer extended repayment terms, particularly for loans used for home purchases.

What happens if I pay off my 401k loan early?

Paying off a 401k loan early generally doesn’t result in penalties. In fact, early repayment can be a smart move to minimize interest accumulation and to replenish your retirement savings sooner.

These answers aim to provide clarity on some of the most common concerns regarding 401k loans. Remember, specific details can vary by plan, so consulting with your plan administrator for personalized information is always a good idea.

Conclusion: Navigating Your Decision on 401k Loans

As we reach the end of our guide on 401k loans, the key takeaway is the importance of balancing immediate financial needs with long-term retirement planning. While 401k loans can provide quick access to funds, the potential impact on your future savings and investment growth is a critical consideration. It’s essential to approach this decision with a comprehensive understanding of both the benefits and risks involved.

Reflect on your current financial situation, the urgency of your needs, and your ability to repay the loan without jeopardizing your retirement goals. Remember, the right financial decision is one that not only addresses your immediate challenges but also aligns with your overall financial well-being.

Take the Next Step with Confidence

Are you considering a 401k loan, seeking further guidance, or exploring other financial options? A financial advisor is ready to assist. Reach out for customized advice that aligns with your unique situation. They can offer the insights and support necessary to make a well-informed choice.

Furthermore, if you possess valuable experiences or insights regarding 401k loans, sharing them could greatly benefit others in similar situations. Partner with a financial advisor to pave the way toward financial stability. Contact a financial advisor today.

Looking for Emergency Funding? Know Your Options

Title Loans Explored: Your Guide to Borrowing Against Your Car

A Safer Route to Quick Cash: Exploring Title Loan Alternatives

Facing a financial crunch often leads to considering a title loan as a quick cash solution. The lure of using your car for immediate funds is strong, but the risks are significant. High interest rates and the danger of losing your vehicle make title loans a precarious choice.

If you’re concerned about these risks, it might be time to look at a safer alternative. Personal loans offer a more secure option. They come with clearer terms and manageable interest rates, and crucially, they don’t put your personal assets at stake.

Choosing a personal loan over a title loan can be a wise decision to avoid unnecessary financial risk. It’s a step towards securing the funds you need without the worry of losing something as valuable as your car. Consider the benefits of a personal loan as a less risky way to meet your financial needs.

|

Wells Fargo Reflect® | 0% APR for 21months (Credit Score 670+)

»

|

iCash Loans | Get a Loan Today

»

|

|

BadCreditLoans.com | Quick Loans up to $10,000

»

|

Brigit | Build Your Credit and Your Savings

»

|

Unlocking the Mystery: Essential Requirements for a Title Loan

When you’re considering a title loan, understanding the essential requirements is crucial. This section breaks down what you need to know to qualify for a title loan, ensuring you’re fully prepared before you apply.

To be eligible for a title loan, there are several key requirements:

- Ownership Proof: You must have a clear, lien-free title to your car. This means no other loans or judgments against the vehicle.

- Vehicle Value: The amount you can borrow largely depends on the value of your car. Lenders typically evaluate the car’s condition, make, model, and mileage.

- Regular Income: Proof of regular income is often required to ensure you can repay the loan. This could be from employment, self-employment, or even social security or disability benefits.

- Valid ID: A government-issued identification, such as a driver’s license, is necessary for identity verification.

- Age Requirement: You must be at least 18 years old to enter into a title loan contract.

These are the basics, but some lenders might have additional requirements. Always check with the lender for their specific criteria to make sure you’re fully equipped for the application process. Understanding these essentials helps you evaluate if a title loan is feasible for you and prepares you for the application steps ahead.

How Much Can I Borrow Against a Car?

Understanding your title loan amount is based on your car’s market value. The value considers factors like make, model, year, and condition. Lenders usually offer 25% to 50% of the car’s value. So, for a car worth $10,000, you might get a loan between $2,500 and $5,000.

Keep in mind that this amount can vary due to state regulations. It’s also vital to consider your ability to repay. Ensure you borrow an amount that aligns with your financial capacity to avoid future financial strain.

The Hidden Pitfalls of Title Loans

Title loans might seem like a quick fix for your financial needs, but it’s essential to be aware of the potential downsides. Understanding these risks can help you make a more informed decision.

The key disadvantages of title loans include:

- High Interest Rates: Title loans often come with exorbitant interest rates, significantly higher than most traditional loans. These rates can quickly escalate the total amount you owe.

- Short Repayment Terms: Typically, title loans have to be repaid within a short period, sometimes as quickly as 30 days. This short repayment window can be challenging for many borrowers.

- Risk of Losing Your Vehicle: If you fail to repay the loan, the lender can repossess your vehicle. Losing your car can not only be inconvenient but also impact your ability to work or manage daily responsibilities.

- Debt Cycle Risk: The combination of high interest rates and short repayment terms can trap borrowers in a cycle of debt. Some find themselves taking out additional loans to repay the original title loan.

Before opting for a title loan, weigh these risks against your immediate financial needs. Sometimes, the long-term financial implications can outweigh the short-term relief provided by the loan. Consider exploring alternative financial solutions that might be less risky and more manageable in the long run.

Do Title Loans Affect Your Credit?

Understanding the impact of a title loan on your credit score is crucial for financial planning. Title loans are typically not reported to credit bureaus since most lenders don’t require a credit check for approval. Therefore, obtaining a title loan won’t directly affect your credit score, nor will your repayments influence it.

However, if you default on the loan and your vehicle is repossessed, this could be reported and negatively impact your credit score. Additionally, if the defaulted loan is transferred to a collection agency, this might also be reported and can significantly harm your credit.

It’s important to consider these potential indirect impacts on your credit when deciding on a title loan. Being aware of all possible outcomes helps you make an informed financial decision.

Understanding Your Options: Auto Equity Loans vs. Title Loans

When considering loans that leverage your vehicle, it’s vital to know the differences between auto equity loans and title loans. Each option caters to different financial situations and comes with its own set of terms.

Auto Equity Loans:

- Based on Vehicle Equity: This loan type considers the equity you have in your car, which is the value of the car minus any outstanding balance on it.

- Credit Check Required: Lenders typically check your credit, as loan terms and eligibility can depend on your credit history and the equity in your vehicle.

- Ongoing Car Payments: It’s possible to get an auto equity loan even if you haven’t fully paid off your car, as long as there’s sufficient equity.

Title Loans:

- Vehicle as Collateral: For a title loan, you must own your car outright. The loan amount is based on the car’s value, without considering any existing car payments.

- No Credit Check: These loans are accessible to those with poor or no credit but often come with higher interest rates.

- Shorter Repayment Terms: Title loans typically have quicker repayment schedules compared to auto equity loans.

By understanding these distinctions, you can better assess which loan type is more suitable for your financial circumstances. Consider the impact on your credit, the loan terms, and how much you can borrow before deciding. Remember, both options involve using your vehicle as collateral, so choosing the right one is key to managing your financial health effectively.

Navigating the Waters: Understanding Title Loan Rates

Understanding title loan rates is crucial due to their high nature. Typically, title loans feature annual percentage rates (APRs) ranging from approximately 100% to 300%. This rate is significantly higher compared to traditional loans.

The high interest means the total amount you need to repay can escalate quickly, making the loan more costly over time. When considering a title loan, it’s important to compare rates from different lenders and calculate the full repayment cost, including all interest charges.

Remember, opting for a loan with a lower interest rate can substantially reduce the overall cost of the loan.

Exploring Alternatives to Title Loans: Balancing Loans and Income Boosters

When you’re looking for quick financial relief, understanding the full range of options, especially alternatives to title loans, is crucial. These alternatives include various loan types and income-boosting strategies.

Loan Options:

- Personal Loans: Generally offer lower interest rates and longer repayment terms, ideal for those with good credit.

- Credit Card Cash Advances: Provide immediate access but come with high interest rates and fees.

- Payday Loans: Offer quick funds but are known for high costs.

- Peer-to-Peer Loans: Feature flexible terms with rates based on your credit profile.

- Home Equity Loans: Use home equity for loans with lower interest rates, but be mindful of the foreclosure risk.

- HELOC (Home Equity Line of Credit): Provides flexible access to funds with variable interest rates, ideal for ongoing expenses.

- 401(k) Loans: Borrow from retirement savings with lower interest rates without a credit check. Remember, there’s a potential impact on retirement funds.

- New Credit Cards with 0% Introductory Offers: Suitable for short-term expenses, offering a period without interest. Be aware of the rates after the introductory period.

- Pawn shop Loans: Provide immediate cash with valuables as collateral. They are quicker and less credit-dependent but come with the risk of losing your items.

|

BadCreditLoans.com | Quick Loans up to $10,000

»

|

Wells Fargo Reflect® | 0% APR for 21months (Credit Score 670+)

»

|

|

iCash Loans | Get a Loan Today

»

|

Brigit | Build Your Credit and Your Savings

»

|

Income Strategies Without Debt:

- Borrowing from Family and Friends: This could offer low- or no-interest loans but may impact personal relationships.

- Selling Personal Items: An effective way to raise funds without taking on debt, though it may require time and effort.

- Seeking Community Assistance: Look into non-repayable financial support from charities or government programs.

- Part-time Work or Side Gigs: Generate additional income through freelance work, side jobs, or gig economy opportunities.

Evaluating both your immediate financial needs and your ability to repay is essential in choosing the right option. Whether it’s a loan tailored to your situation or an alternative income source, careful consideration will help maintain your financial stability while addressing your current needs.

Conclusion: Navigating Title Loans and Their Alternatives

In conclusion, while title loans offer a quick financial solution, they carry significant risks and high costs. It’s essential to carefully consider these drawbacks, such as potentially exorbitant interest rates and the risk of vehicle loss, against your immediate financial needs.

Often, safer alternatives like personal loans, credit card advances, or borrowing from family might be more sustainable choices. Exploring these options, along with ways to generate additional income, can provide the necessary financial support without the heavy burdens of title loans.

Making an informed decision that balances your immediate needs with long-term financial health is key to maintaining financial stability and peace of mind.

Secure Your Financial Future

If you’re considering alternatives to a title loan, applying for a personal loan might be your best option. We offer tailored loan solutions to fit your specific financial needs.

Moving Forward with Confidence

The financial decisions you make today shape your future. For expert advice tailored to your unique needs, consult a financial advisor. Their guidance can help you make well-informed choices.

Your experiences with loans could enlighten others. Consider sharing your story to assist those facing similar decisions.

Need Emergency Funding? Discover Your Options

Mastering Credit Cards: Types, Benefits, and Strategic Use

Need Cash Fast? Understanding Credit Card Solutions

In moments when emergency funds are critical, the search for quick financial relief becomes a pressing concern. Navigating through the maze of credit card options can be daunting, especially when urgency meets the need for a wise decision.

The Challenge: Finding immediate funds often leads to hasty choices, potentially compounding financial stress.

The Solution: Credit cards can be a swift source of emergency cash, but selecting the right one is key to managing your financial health.

Dive deeper with us as we explore how to effectively use credit cards for emergency funds, ensuring you make informed choices that support your financial well-being.

Credit Card Essentials: From Selection to Payment

When choosing a credit card, understanding its various components is crucial. This guide outlines key aspects from initial considerations to making payments, including types of fees and specific features to be aware of.

Initial Considerations:

Credit Requirements: Different cards have varying credit score requirements, from secured and student cards for building credit to premium cards requiring high credit scores.

Interest Rates (APR): The annual percentage rate affects how much you’ll pay in interest if you carry a balance.

Grace Period: The time between the end of your billing cycle and the due date. Paying your balance in full within this period can avoid interest charges.

Fees and Additional Costs:

Annual Fees: Some cards charge a yearly fee for usage, often offset by rewards or benefits.

Late Payment Fees: Fees incurred for not making the minimum payment by the due date.

Balance Transfer Fees: Charged when transferring a balance from one card to another, usually a percentage of the transferred amount.

Foreign Transaction Fees: Fees for transactions made in a foreign currency or through a foreign bank.

Cash Advance Fees: Charged for using your credit card to withdraw cash, either a flat fee or a percentage of the advance.

Making Payments:

Minimum Payment: The least amount you can pay by the due date to keep the account in good standing, usually a small percentage of your total balance.

Full Payment: Paying the full statement balance each month to avoid interest charges.

Automatic Payments: Setting up auto-pay can ensure you never miss a payment, protecting your credit score.

Card Features and Benefits:

Rewards Programs: Offers like cash back, points, or travel miles based on your spending.

Security Features: EMV chips and contactless payments enhance security, reducing the risk of fraud.

Benefits: Additional perks such as extended warranties, travel insurance, and airport lounge access.

Understanding these components can help you navigate the complexities of credit cards, from choosing the right card to managing payments wisely.

Navigating Credit Cards: Find Your Perfect Match

Credit cards come in various forms, each designed to cater to different financial needs and preferences. Here’s a quick rundown of the primary types you’ll encounter:

- Secured Credit Cards: Require a security deposit which usually sets your credit limit, ideal for building or rebuilding credit.

- Student Credit Cards: Designed for college students new to credit, often with educational resources and lower limits.

- Low-Interest Credit Cards: Offer lower ongoing APRs, beneficial for those who might carry a balance but still require a fair credit score.

- Balance Transfer Credit Cards: Feature low or 0% APR introductory offers on balance transfers, suited for consolidating debt, usually needing a good credit score.

- Rewards Credit Cards: Provide cash back, points, or miles on purchases, requiring good to excellent credit for the best rewards rates.

- Travel Credit Cards: Target frequent travelers with perks like miles and free hotel stays, demanding a good to excellent credit score for valuable benefits.

- Business Credit Cards: Offer rewards and benefits tailored to business expenses, requiring a good to excellent credit history to qualify for the best offers.

This progression reflects the journey from establishing credit through managing and consolidating debt to maximizing rewards and benefits as your credit score and financial management skills improve.

FAQ: Navigating Your Credit Card Concerns

What credit card is the easiest to get?

Secured credit cards are typically the easiest to obtain. They require a security deposit that serves as your credit limit, minimizing the issuer’s risk.

What are instant approval credit cards?

Instant approval credit cards offer a quick decision on your application, often within minutes. They’re ideal for those who meet the issuer’s credit criteria and need immediate credit access.

What should I use my credit card for to build credit?

Using your credit card for regular, small purchases and paying the balance off in full each month is a solid strategy to build credit. This demonstrates responsible credit use without accruing interest.

Should I pay off my credit card in full or leave a small balance?

Paying off your credit card in full each month is advisable. Contrary to some myths, carrying a balance does not improve your credit score and results in unnecessary interest charges.

How often should I check my credit card statement?

Regularly reviewing your credit card statement, ideally monthly, is crucial. This practice helps catch any unauthorized transactions or errors promptly and ensures you’re aware of your spending and due payments.

Empowering Your Credit Card Choices

In navigating the complexities of credit cards, from selecting the right type for your needs to understanding the intricacies of their use, our journey has highlighted the importance of informed decision-making. Credit cards are powerful financial tools that, when used wisely, can enhance your financial flexibility, offer valuable rewards, and assist in building a robust credit history.

The key is to approach credit card usage with knowledge and responsibility, ensuring that your choices align with your financial goals and circumstances. Whether you’re looking for immediate financial assistance, aiming to build credit, or seeking to maximize rewards, the right credit card can make a significant difference in your financial strategy.

Seek Expert Guidance

As you consider your next steps, remember that expert advice can further demystify the credit card selection process and tailor your choices to your personal financial landscape. Consult with a financial advisor to explore your options thoroughly and make choices that best suit your financial future.

Ready to Apply?

Find your perfect credit card match from the curated list below. Click on the card that interests you to start your application process. Your journey towards effective credit usage and financial empowerment is just a click away.

Credit Card Cash Advances: Emergency Funds When You Need Them Most

In times of financial emergencies, securing swift access to funds is paramount. Credit card cash advances stand out as a rapid solution, offering instant cash from your available credit line. Facing situations like unexpected medical expenses, crucial home repairs, or last-minute emergencies can be less daunting with the option to quickly convert part of your credit limit into cash.

However, the convenience of cash advances comes with the need for careful consideration. It’s vital to understand their impact on your credit, the terms attached, and effective repayment strategies. This guide is designed to provide you with a comprehensive understanding of credit card cash advances, helping you to utilize this option effectively while safeguarding your financial well-being.

Understanding Credit Card Cash Advances?

A credit card cash advance allows you to withdraw cash from your credit limit. Accessible via ATMs, banks, or convenience checks, it offers quick funds for emergencies.

However, it carries higher interest rates and fees, with interest accruing immediately. Due to these costs, using cash advances cautiously and planning for quick repayment is essential.

Navigating the Costs of Cash Advances

When considering a credit card cash advance, it’s essential to understand the financial implications.

- Interest Rates: The interest rate for cash advances is often higher than that for purchases. While the exact rate varies by credit card issuer, it can range from about 20% to 30% APR or even higher, depending on your credit card terms and creditworthiness.

- Transaction Fees: Cash advance fees typically range from 3% to 5% of the total amount withdrawn, with many credit card issuers setting a minimum fee amount, such as $10.

The Impact of Cash Advances on Your Credit

Taking a cash advance from your credit card can influence your credit health in several ways. Here’s a concise look at its potential impact:

Credit Utilization: Cash advances increase your credit utilization ratio—the amount of credit you’re using compared to your credit limit. A higher ratio can negatively affect your credit score, as it indicates higher usage of available credit.

Debt Accumulation: Frequent reliance on cash advances may lead to accumulating debt, which can become challenging to manage, potentially leading to missed payments or high balances that hurt your credit score.

Inquiries and New Debt: While the act of taking a cash advance doesn’t directly result in a hard inquiry on your credit report, the increased debt and potential for higher utilization can indirectly influence your creditworthiness.

Responsible use of cash advances, with an understanding of their impact on your credit and a plan for quick repayment, can help mitigate negative effects. However, considering alternatives with lower costs and less impact on your credit utilization is often advisable.

Is Credit Card Cash Advances Right for You?

Deciding whether to use a credit card cash advance involves weighing the advantages and disadvantages and considering alternative financial solutions.

Pros

- Immediate Access to Funds: Cash advances provide quick cash in emergency situations.

- Convenience: Easily accessible through ATMs or bank withdrawals.

- No Collateral Required: Unlike some loans, cash advances don’t require collateral.

Cons

- High Interest Rates: Cash advances typically have higher interest rates than regular credit card purchases.

- Additional Fees: Expect transaction fees, ATM fees, and sometimes, a higher interest rate from the day of the transaction.

- No Grace Period: Interest accrues immediately, increasing the overall repayment amount.

Making an Informed Decision on Cash Advances

Credit card cash advances offer immediate access to funds, presenting a quick solution for urgent financial needs. Yet, their high interest rates and fees necessitate careful consideration. It’s vital to understand the details of cash advances, including their financial implications, and view them as a last resort for emergencies after exploring all other options.

Seek Financial Advice

Considering a cash advance? Consulting with a financial advisor can provide valuable insights, helping you to evaluate your situation and alternative financial solutions. This guidance ensures that any decision to proceed with a cash advance is well-informed and in harmony with your broader financial strategy.

Remember, thorough exploration of alternatives and informed decision-making are crucial steps toward maintaining financial stability.

Discover More Fast Cash Options

Home Equity Loans Explained: Unlocking Your Home’s Financial Power

Exploring the Mechanics of Home Equity Loans

Home equity loans offer a structured way to access the financial value tied up in your home. This type of loan transforms the equity you’ve accumulated into a tangible resource for a range of financial needs. Here’s how it typically unfolds:

- Step 1: Assessing Your Equity

Start by determining the amount of equity in your home. This is the difference between your property’s current market value and any outstanding mortgage balance. The higher your equity, the more you may be eligible to borrow.

- Step 2: Understanding Loan Terms

Home equity loans have fixed terms, typically spanning five to 30 years. This fixed term comes with a set repayment schedule, making it easier to plan your finances.

- Step 3: Getting to Know Interest Rates

These loans are known for their fixed interest rates. This means the interest rate remains constant throughout the loan period, ensuring your monthly payments are predictable.

- Step 4: Applying the Loan

You can utilize the loan for a variety of purposes. Common uses include funding home renovations, consolidating high-interest debt, covering educational expenses, or addressing major medical bills.

By taking a systematic approach to understanding home equity loans, you can better gauge whether this financial tool suits your specific needs and objectives. It’s a blend of strategic planning and financial insight, aimed at optimizing the value of your home investment.

Pawn Shop Loans Unlocked: Your Ultimate Guide to Quick Cash and Smart Borrowing

Hooked on Cash? Discover the Quick Fix of Pawn Shop Loans

In an instant, financial emergencies can disrupt our peace of mind, casting us into a sea of uncertainty. Whether it’s an unexpected bill, a sudden repair, or a personal crisis, the scramble for quick cash becomes inevitable. Yet, the quest for immediate funds often hits a wall – traditional lending routes like banks and credit unions demand time and a squeaky-clean credit history, leaving many out in the cold.

Enter the world of pawn shop loans, a beacon of hope for those seeking an immediate financial lifeline without the dread of credit checks. But as with any quick fix, it’s crucial to peel back the layers and understand what you’re diving into. This guide is your flashlight in the murky waters of pawn shop borrowing, revealing how these loans work, their benefits, and the pitfalls to avoid. We’ll also explore the ultimate dilemma: to pawn or to sell. Plus, for those moments when repayment seems like a distant dream, we uncover what happens next.

Armed with knowledge, you’ll navigate the pawn shop loan maze with confidence, ensuring your financial decision is not just quick but also smart and informed. Let’s demystify the process, weigh the options, and unlock the secrets to using pawn shop loans to your advantage.

The Secret World of Pawn Shop Loans Unveiled

Pawn shop loans often fly under the radar in the world of finance, yet they’re a cornerstone for many seeking immediate financial relief. At their core, these loans are a straightforward exchange – your valuable items for instant cash. But what makes them particularly appealing is the absence of credit checks, making them accessible to virtually anyone with something of value.

How Do Pawn Shop Loans Work?

A pawn shop loan is, in essence, a secured loan. The collateral? Anything from a vintage guitar and high-end electronics to jewelry. The process is simple: you bring in your item, and the pawnbroker appraises its value and offers you a loan based on a percentage of that value. Interest rates and loan terms can vary widely, so it’s critical to understand the specifics upfront.

One of the most compelling aspects of pawn shop loans is their speed. Unlike traditional bank loans, which can take days or weeks to process, pawn shop transactions can be completed in minutes. This immediacy can be a lifeline in times of financial distress.

However, the convenience of pawn shop loans comes with its considerations. The loan amount you receive is often significantly lower than the actual value of your item, and interest rates can be high. It’s this combination that necessitates a deeper dive into how pawn shop loans work, ensuring you’re making an informed decision when you need cash fast.

In the next section, we’ll step through the pawn shop loan process, providing you with a roadmap to navigate this quick-cash solution with your eyes wide open.

Unlocking Cash with Your Valuables: A Step-By-Step Guide

- Select Your Collateral: Identify a valuable item you own, such as jewelry, electronics, or musical instruments, that you’re willing to use as collateral for a loan.

- Find a Reputable Pawn Shop: Research to choose a pawn shop known for fair dealings and cheerful customer reviews to ensure you get the best possible terms.

- Get Your Item Appraised: Present your item for appraisal at the pawn shop. The loan offer will be based on the item’s current market value, condition, and the pawn shop’s ability to sell the item if necessary.

- Understand the Loan Terms: Carefully review the loan amount, interest rate, fees, and repayment period (usually 30 to 90 days) offered by the pawnbroker. Make sure you fully understand and agree to these terms before proceeding.

- Receive Cash: Upon agreement, you’ll provide the item as collateral and receive the loan amount in cash. Ensure you receive a pawn ticket or receipt that details your loan terms and is required to reclaim your item later.

- Repay the Loan: Repay the loan amount plus any accrued interest and fees by the end of the loan term to reclaim your collateral. If you’re unable to repay in time, inquire about the possibility of extending or renewing the loan.

- Non-Repayment Consequences: If repayment is not possible, the pawn shop retains the right to sell your item. However, this transaction does not impact your credit score, as pawn loans do not require credit checks.

This streamlined guide is designed with you in mind, offering a clear path through the process of securing and managing a pawn shop loan. By understanding each step, you’re empowered to make choices that align with your financial needs and circumstances. Whether you’re navigating a tight financial spot or seeking a quick cash solution, this guide aims to equip you with the knowledge to make informed and beneficial decisions.

Why Pawn Shop Loans Could Be Your Financial Knight in Shining Armor

When cash flow problems arise, pawn shop loans can be a swift and efficient solution, offering several advantages that make them an attractive option for many. Here’s why considering a pawn shop loan might just be the financial rescue you need:

1. Speed: One of the most significant benefits of pawn shop loans is the rapid access to cash. Unlike traditional bank loans that take days or weeks to process, pawn shop transactions can be completed within minutes, providing immediate financial relief.

2. No Credit Checks: Pawn shop loans do not require a credit check. This means your credit score won’t be impacted by applying for a loan, and you won’t be denied based on your credit history. This feature is particularly beneficial for those with less-than-perfect credit or those who wish to avoid inquiries that could lower their credit scores.

3. Flexibility: The loan amount is based on the value of your collateral, not your creditworthiness or income. This can provide more flexibility in the amount you can borrow, especially if you have valuable items but are limited by a low credit score or lack of verifiable income.

4. Confidentiality: Pawn shop loans offer a high level of privacy. There’s no need to disclose personal financial information or reasons for needing the loan, which can be a relief for those who prefer to keep their financial matters private.

5. Simple Repayment: Repaying a pawn shop loan is straightforward. If you can’t repay the loan by the end of the term, you can choose to surrender the collateral without the worry of debt collectors or negative marks on your credit report. For many, this clear-cut outcome removes the anxiety of potentially spiraling into further debt.

Pawn shop loans aren’t without their drawbacks, such as potentially high interest rates and the risk of losing your collateral. However, for those in need of quick cash without the hassle of credit checks or lengthy approval processes, they offer a viable and immediate solution. Understanding these benefits can help you decide if a pawn shop loan is the right choice for your financial situation.

Pawn Shop Loans: Weighing the Pros and Cons

Pawn shop loans can be a convenient solution for immediate financial needs, offering both benefits and drawbacks. Here’s a closer look at what to consider:

Advantages of Pawn Shop Loans:

- Speed: Quick access to cash, often within minutes, is a primary advantage for urgent financial needs.

- No Credit Checks: These loans are accessible without a credit check, making them available to those with poor or no credit history.

- Flexibility: The loan amount is based on the collateral’s value, not the borrower’s creditworthiness or income.

- Confidentiality: The process is private, requiring no disclosure of financial details or reasons for the loan.

- Simple Repayment: If unable to repay, the borrower can forfeit the collateral without further debt consequences or impacts on credit score.

Considerations and Risks:

- Higher Costs: Pawn shop loans can carry higher interest rates and fees compared to traditional lending options.

- Risk of Losing Collateral: Failure to repay the loan results in losing the pawned item, which could have both financial and sentimental value.

- Short Repayment Terms: Typically, loans have a short repayment duration, potentially adding pressure to repay quickly.

- Potential for a Debt Cycle: There’s a risk of entering a cycle of debt if continually relying on pawn loans for financial needs.

- Loan Amount Limitations: The loan amount is usually much lower than the actual retail value of the pawned item, limiting the cash available to the borrower.

By understanding the full spectrum of pros and cons, borrowers can navigate pawn shop loans more wisely, ensuring these financial tools serve their needs without unforeseen drawbacks.

Does Pawning Hurt Your Credit? The Surprising Truth

Pawn shop loans offer a unique advantage for those concerned about their credit scores—they don’t require a credit check, nor do they impact your credit score. This feature ensures that applying for a pawn shop loan won’t lower your credit score, as there’s no inquiry reported to credit bureaus.

The loan is secured with collateral, meaning if you can’t repay, the pawn shop simply keeps the item you pawned. This setup avoids the negative impact on your credit history that can come from other types of loans. However, while your credit score remains unaffected, it’s crucial to consider the potential loss of your pawned item. This loss is the main risk of using pawn shop loans, highlighting the need to balance the immediate financial benefit against your collateral’s sentimental or monetary value.

Is It Better to Sell or Get a Loan at a Pawn Shop?

Selling to a Pawn Shop:

Selling items to a pawn shop offers immediate cash without the future obligation of repayment, making it an appealing option for those in need of quick funds. This approach often results in a higher cash payout compared to the loan value of the same items, providing a straightforward financial boost without concerns about interest or fees.

Opting for a Loan:

Choosing a loan instead allows you to retain ownership of your items, offering a temporary financial solution with the opportunity to reclaim your belongings once the loan is repaid. This option is especially suitable for items of sentimental value or when you anticipate being able to cover the loan plus interest in the near future.

Key Considerations:

The choice between selling and loaning hinges on several factors, including the immediate need for cash, the sentimental value of the items, and your financial stability to repay a loan. Selling provides a no-strings-attached way to address financial needs, while loans offer a way to retain your valuables potentially. Assessing the importance of the item, the feasibility of repaying a loan, and the urgency of your financial needs will help guide the decision that best suits your situation.

What Happens If You Can’t Pay Back a Pawn Loan?

If you can’t repay a pawn shop loan, the shop can sell your collateral. This won’t affect your credit score, as pawn loans aren’t reported to credit bureaus.

Pawn shops may allow you to extend or renew the loan by paying the accrued interest, but this increases the overall cost due to additional interest and fees.

Before opting for a pawn loan, consider your ability to repay and the value of the item to avoid losing something important. Carefully review the loan terms and assess your financial situation.

Navigating Your Financial Options: Loans vs. Income Strategies

When faced with the need for quick financial assistance, it’s crucial to explore and understand the spectrum of options available. These can be broadly divided into immediate financial solutions through loans and strategies to increase income without incurring debt.

Immediate Financial Solutions:

- Payday Loans: Immediate, but often come with high costs.

- Personal Loans: Lower interest for those with good credit, requiring proof of repayment ability.

- Credit Card Cash Advances: Accessible but expensive in terms of interest and fees.

- Title Loans: Quick cash with your vehicle at stake.

- Peer-to-Peer Loans: Flexible, community-based lending with varying rates.

- Home Equity Loans: Lower interest rates and higher loan amounts based on home equity. Require a longer approval process and carry the risk of foreclosure.

- HELOC (Home Equity Line of Credit): Offers a flexible funding stream with variable interest rates, suited for continuous financial needs.

- 401(k) Loans: Borrow from your retirement savings with no credit check, lower rates, and no taxes if repaid promptly. Risks include potential impact on retirement funds and penalties for non-repayment.

- Getting a New Credit Card: Beneficial for 0% introductory interest offers on purchases or balance transfers, providing a cost-effective way to manage short-term expenses. It is important to consider the regular interest rate post-introductory period and the potential impact on credit scores.

|

BadCreditLoans.com | Quick Loans up to $10,000

»

|

Wells Fargo Reflect® | 0% APR for 21months (Credit Score 670+)

»

|

|

iCash Loans | Get a Loan Today

»

|

Brigit | Build Your Credit and Your Savings

»

|

Income Strategies Without Debt:

- Borrowing from Family and Friends: Personal, potentially interest-free loans with relationship considerations.

- Selling Personal Items: A slower, effort-intensive option that converts belongings into cash.

- Seeking Community Assistance: Non-repayable support from charities or government programs for those in financial distress.

- Exploring Side Gigs: Earning extra income through part-time work or freelancing.

Understanding the nature of your financial needs and your ability to meet repayment obligations will help you choose the most appropriate path. Whether it’s through a loan that matches your repayment capacity or a strategy to enhance your income without the burden of debt, careful consideration will safeguard your financial health while addressing your immediate needs.

Smart Borrowing: Master the Art of Pawn Shop Loans

Navigating the waters of pawn shop loans requires a keen understanding of both the process and the strategies to ensure you’re making the most informed decision possible. Here’s how you can approach pawn shop loans smartly, safeguarding your financial interests while meeting your immediate cash needs:

- Assess the Need and Value: Ensure the item’s cash value outweighs its sentimental or financial importance to you.

- Know the Terms: Fully understand interest rates, fees, and repayment terms before committing.

- Negotiate: Don’t hesitate to negotiate for better loan terms or amounts.

- Have a Repayment Plan: Plan how you’ll repay the loan and interest before taking it.

- Explore Alternatives: Consider other financial options before opting for a pawn loan.

- Be Ready to Walk Away: Don’t proceed with the loan if terms aren’t favorable or repayment is uncertain.

Conclusion: Navigating Financial Options Beyond Pawn Shop Loans

Understanding pawn shop loans is crucial, but it’s equally important to consider all your financial options carefully. Before deciding, thoroughly evaluate the loan’s terms, including interest rates and repayment schedules, and ensure you have a solid plan for repayment.

If you’re unsure about the best path forward or if pawn shop loans seem like your only option, it might be time to consult with a financial advisor. A professional can offer personalized advice and help you explore alternatives that align with your financial goals and situation.

Remember, making informed financial decisions is key to maintaining your financial health. If a pawn shop loan doesn’t fit your needs, contact a financial advisor today. With their guidance, you can find a solution that supports your journey to financial stability and success.

Peer-to-Peer Lending for Bad Credit: Unlocking Financial Opportunities

Facing financial hurdles can be daunting, especially when a less-than-perfect credit score closes the doors to traditional financing options. When banks turn you away, you’re left wondering how to cover unexpected bills or fund essential purchases. This is a common predicament for many, but there’s a solution that’s gaining traction: peer-to-peer (P2P) lending.

P2P lending offers a direct bridge between borrowers and investors, cutting through the red tape of conventional banking. It shines as a beacon of hope for those with bad credit, providing an accessible avenue to secure the funds you need without the stringent requirements of traditional lenders.

This innovative approach facilitates the financial support you seek and presents an opportunity to rebuild your credit score through consistent, timely repayments. Throughout this guide, we’ll delve into the workings of peer-to-peer lending for individuals with bad credit, offering you the tools and knowledge to navigate this option with confidence and improve your financial standing.

Understanding Peer-to-Peer Lending

Peer-to-peer lending revolutionizes how individuals borrow and lend money by facilitating direct financial transactions between peers, bypassing traditional banking institutions. This model not only democratizes lending but also opens doors for those who conventional financial systems might sideline due to bad credit.

How It Works

At its core, P2P lending platforms connect borrowers needing funds with investors willing to lend their money in exchange for interest payments. This direct lending approach often results in more favorable terms for both parties, as it cuts out the middleman and the overhead costs associated with traditional banks.

Why It’s Suitable for Bad Credit

- Tailored Risk Assessment: P2P platforms use innovative risk assessment methods that go beyond traditional credit scores, considering other factors that demonstrate a borrower’s reliability.

- Competitive Interest Rates: Even with bad credit, borrowers can often find more competitive rates compared to high-interest bank loans or credit cards.

- Flexible Terms: Many P2P lenders offer more flexible repayment terms, making it easier for individuals with varying financial situations to find a loan that fits their needs.

Getting Started

Starting your journey with P2P lending involves creating a profile on a lending platform, submitting a loan application detailing how much you need and for what purpose, and then waiting for approval from potential investors. It’s a process that values transparency and personal stories, allowing borrowers to explain their financial situations and goals directly to lenders.

The Appeal of P2P Lending for Bad Credit

Peer-to-peer lending stands out as a beacon of hope for those who find themselves with a bad credit rating. Its unique approach to lending and borrowing brings several benefits that traditional financial institutions often cannot match, especially for those who have faced financial challenges in the past.

Accessibility

Unlike traditional banks that rely heavily on credit scores, P2P lending platforms often employ a more holistic approach to borrower evaluation. This accessibility opens up new avenues for individuals who need financial assistance but are hindered by their credit history.

Competitive Rates

P2P lending can offer more competitive interest rates compared to other bad credit loan options. The rates are determined by the market and the individual’s risk profile, giving borrowers a fair chance to secure affordable loans.

Personalized Experience

The P2P lending process allows borrowers to present their case directly to potential lenders, making it a more personalized and humanized experience. This direct connection can lead to better understanding and empathy for borrowers’ situations, often leading to more favorable loan terms.

Quick and Simple Process

The online nature of P2P lending platforms streamlines the application and funding process, making it faster and more convenient than traditional loan applications. This efficiency is particularly beneficial for those in urgent need of funds.

How to Access P2P Loans with Bad Credit

Securing a peer-to-peer loan with bad credit might seem daunting, but with the right approach and preparation, it’s entirely possible. Here’s how you can improve your odds of approval and access the funds you need through P2P lending platforms.

- Craft a Compelling Application: Your loan application is your first impression of potential lenders. Highlight any aspects of your financial situation that show stability or improvement, such as a steady income or successful debt repayments. Be transparent about your credit history, but focus on your plan for using and repaying the loan.

- Enhance Your Credit Profile: Even slight improvements in your credit score can significantly impact your loan terms. Consider taking steps to improve your credit, such as paying down existing debt or correcting errors on your credit report, before applying.

- Choose the Right Platform: Different P2P lending platforms cater to various borrower profiles. Research platforms that are known to be more accommodating to individuals with bad credit and read reviews from other borrowers.

- Consider a Co-Signer: Some P2P platforms allow you to apply with a co-signer. Having someone with a stronger credit score co-sign your loan can increase your chances of approval and possibly secure you a lower interest rate.

- Be Realistic and Honest: Set realistic borrowing amounts that align with your ability to repay. Overborrowing can lead to rejection or financial strain down the line. Honesty about your financial situation and clarity about how you plan to use and repay the loan can build trust with potential lenders.

Selecting the Right P2P Platform

Choosing the right peer-to-peer lending platform is crucial for securing a loan, especially when you have bad credit. Each platform has its own set of rules, interest rates, and borrower requirements. Here’s how to ensure you select the platform that’s right for you.

Research Platform Reputations

Start with thorough research. Look for platforms with positive reviews, especially from borrowers with similar credit profiles to yours. Check for any complaints filed against the platform and how those complaints were resolved.

Compare Interest Rates and Fees

Interest rates and fees can vary significantly from one P2P platform to another. While bad credit might mean higher rates, some platforms specialize in loans for borrowers with less-than-perfect credit and offer competitive rates.

Understand the Loan Terms

Carefully review the loan terms offered by different platforms. Pay close attention to loan duration, repayment options, and any penalties for late or early payments.

Check Eligibility Requirements

Some platforms have specific eligibility requirements for borrowers. Ensure you meet these criteria before applying to avoid wasting time on a platform that won’t serve you.

Evaluate the Application Process

Consider the ease and speed of the application process. A user-friendly platform that provides quick responses can be crucial if you need funds urgently.

Risks and Considerations in P2P Lending for Bad Credit

While peer-to-peer lending offers a valuable financial lifeline for those with less-than-ideal credit scores, it’s important to approach this option with a clear understanding of the potential risks involved. Here’s what you need to consider:

- Higher Interest Rates: Borrowers with bad credit may face higher interest rates on P2P loans compared to those with better credit profiles. It’s crucial to assess whether the loan’s cost is manageable within your budget.